Smart Money App Plum Reaches Profitability

Hey Digital Banking Fanatic!

In a sign that the "growth-at-all-costs" era is firmly over, UK smart money app Plum has reached operational profitability for the first time, hitting positive EBITDA in January 2026 after scaling to £3bn in assets and 5m+ downloads.

Fueled by AI-powered savings like high-yield Cash ISAs and diversified revenue streams, Plum exemplifies how "smart money" apps are evolving into sustainable financial hubs.

“We’ve worked very hard on our product to make sure it continues to deliver outstanding benefits for customers. This has paid off as we’ve now reached operational profitability, a key milestone for any company but especially for a fast-growing FinTech like us,” said Victor Trokoudes, founder and CEO at Plum.

This milestone echoes broader FinTech maturation: Monzo's £113m+ profits since 2023, Starling's steady gains since 2021, Revolut's £790m 2024 net profit, and global flips like Nubank ($2bn income) and Klarna ($120m).

As neobanks and personal finance tools prove scalable economics, expect more incumbents to face AI-native challengers delivering real returns, not just users.

Victor Trokoudes, former Head of International & Banking at Wise, also said that Plum can now reinvest the profit back into the app, citing the ‘huge opportunity’ offered by generative AI in helping people manage their finances.

Dive deeper into digital banking's latest moves below. Catch you tomorrow!

Cheers,

INSIGHTS

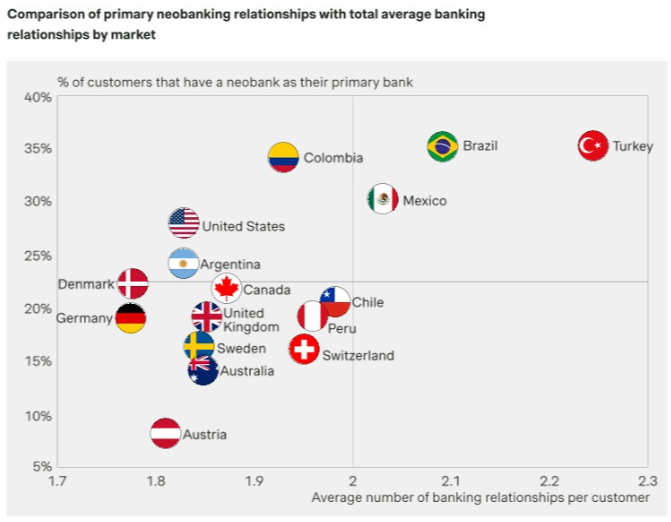

➡️ Neobanking beyond disruption by Simon-Kucher.

NEWS

🇬🇧 Smart money app Plum reaches profitability. Plum has reported strong financial growth of 60%+ year on year, along with making £34m in annual recurring revenue (ARR). The app has multiple income streams spanning customer subscriptions, asset-based revenue, and transaction revenue, which have together contributed to the company achieving the milestone.

🇺🇸 Customers Bank taps OpenAI for banking transformation. The collaboration aims to accelerate the deployment of artificial intelligence across its commercial banking operations, marking a significant step toward becoming an AI-native financial institution.

🇧🇷 Nubank to invest R$ 45 billion in Brazil in 2026. The invested amount will support AI-driven platforms, new financial products, infrastructure expansion, and lending capacity. The move reinforces its long-term commitment to its largest market, where it serves over 113 million customers.

🇪🇸 Revolut integrates Catalan into ATMs, web, and app for its 1.2 million customers. Revolut is expanding rapidly in Catalonia, rolling out Catalan language support across its ATMs, website, and app by 2027. The company is also scaling its ATM network in Spain with plans to reach up to 200 machines nationwide. Additionally, the FinTech neobank is to open its first physical store in Barcelona. The project is still in its early stages, and the company said the opening timeline would depend on construction progress.

🇫🇷 Qonto transforms into an AI-native FinTech, deploying two intelligent agents across 600,000 businesses. The Operator and The Analyst can execute routine banking operations through natural language requests, eliminating the manual work that currently costs SMEs up to 8 hours per week.

🇺🇸 Q2 Enhances account takeover protection with AI-enabled detection and real-time response capabilities. The solutions enable continuous monitoring across the digital banking journey, allowing financial institutions to identify threats earlier and respond more effectively.

🇮🇳 Flipkart, Axis Bank, and PayU launch biometric card payments in India. Customers can complete purchases through issuer-level biometric verification, reducing dependence on SMS-based OTPs that can create delays, failed transactions, and added checkout friction.

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.