Allica testing agentic AI system for loans

Hey Digital Banking Fanatic!

We always knew AI would get here eventually, and it's happening faster than most expected.

British SME challenger bank Allica has just gone live with an end-to-end agentic AI system test that takes an unstructured email loan application, assesses it, and returns a credit decision within minutes. Zero humans in the loop.

The agent is already running in production with two of Allica's largest broker firms, handling around 10% of their email-submitted lending applications. In its initial production phase, 50% of cases were auto-decisioned end-to-end.

Remember when Klarna's CEO announced he'd replace customer support staff with AI, and half the industry scoffed? Within months, others were quietly doing the same.

The real question isn't whether banks, established or challenger, will deploy their own loan-decisioning agents. It's how much longer they can afford to wait.

Check everything else going around the digital banking's latest moves below. See you tomorrow!

Cheers,

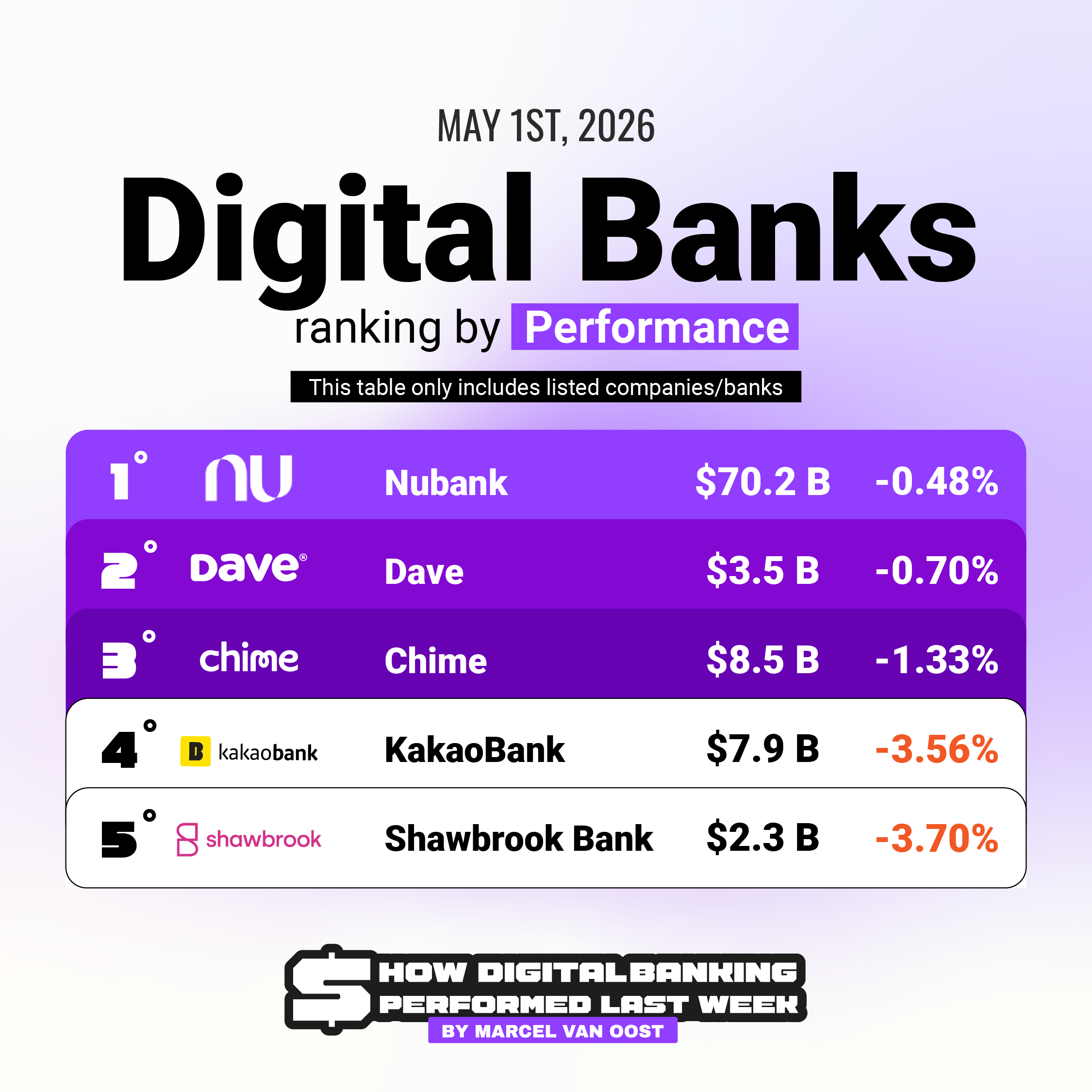

HOW DIGITAL BANKING PERFORMED LAST WEEK

📈 Top 5 Digital Banks Listed on Stock Exchanges by Weekly Performance📉

Here are the big movers of the week:

NEWS

🇳🇱 Mastercard and Rabobank completed the Netherlands’ first AI agent payment, where an assistant booked an experience via Priceless.com using Agent Pay. The system keeps card data hidden, relies on user consent and passkeys, and signals a shift toward secure, AI-driven commerce.

🇬🇧 Allica Bank is testing an agentic AI system that processes SME loan requests from email to credit decision in an average of 12 minutes, with no human input. Live across key brokers, it auto-decided 50% of cases, aiming to speed up complex lending while broader AI adoption expands internally.

🇧🇷 Nubank has launched Vantagens Nu, a new in-app hub for cashback, coupons, and partner deals, including recurring offers with Shopee. The feature centralizes rewards, making benefits easier to access as Nubank expands everyday value for users.

🇺🇸 Slash Financial has launched Global Cards, enabling international businesses to spend in USD without a U.S. entity. Powered by Visa and Rain’s stablecoin infrastructure, the product extends Global USD accounts, simplifying cross-border spend and reducing FX and setup friction.

🇳🇱 Monzo completed acquisition of Habito, integrating end-to-end mortgage broking into its app. The deal strengthens Monzo’s homeownership offering, combining tracking tools with in-app mortgage services as it expands beyond core banking.

🇲🇽 Belvo and Banco Plata partner to expand credit access in Mexico using Open Finance and employment data. The integration enables real-time income verification and automated repayments, improving approvals and reaching underserved users with limited credit history.

GOLDEN NUGGET

𝗪𝗵𝗮𝘁 𝗶𝘀 𝗶𝗻𝘁𝗲𝗿𝗰𝗵𝗮𝗻𝗴𝗲, 𝗮𝗻𝗱 𝘄𝗵𝗮𝘁 𝗳𝗮𝗰𝘁𝗼𝗿𝘀 𝗶𝗺𝗽𝗮𝗰𝘁 𝘁𝗵𝗲 𝗶𝗻𝘁𝗲𝗿𝗰𝗵𝗮𝗻𝗴𝗲 𝗿𝗮𝘁𝗲?

Let’s break it down:

Every time a consumer swipes a card to make a purchase, the merchant pays an interchange fee.

Revenue from the fee gets divided among parties that facilitated the transaction: the banks that send and receive the payment, the card network, the payment processor, and—more recently—FinTechs and businesses that embed payments.

When you take the bird-eye view diagram above as an example:

If a user swipes a card issued by a Neobank, $1.70 (interchange fee) goes to the issuing bank and the card network, $0.50 (acquiring fee) goes to the acquiring bank.

Interchange fees are not always the same though.

𝗪𝗵𝗮𝘁 𝗳𝗮𝗰𝘁𝗼𝗿𝘀 𝗶𝗺𝗽𝗮𝗰𝘁 𝗶𝗻𝘁𝗲𝗿𝗰𝗵𝗮𝗻𝗴𝗲 𝗿𝗮𝘁𝗲?

► Credit vs. Debit

Interchange rates on credit cards are significantly higher than those on debit cards.

► Rewards programs

These benefits are financed through higher interchange rates, and have proven to be very popular with consumers.

► Online vs. Offline

Online purchases are less secure than in-person purchases.

► Consumer vs. Commercial

Cards associated with business or corporate accounts carry higher interchange rates than consumer cards.

► Merchant Category Code (MCC)

Every merchant is categorized by the major card networks according to a Merchant Category Code (MCC). This means that there are different interchange rates depending on whether someone uses a card in a supermarket, a retail store, a gas station, or with some other form of merchant.

► The Card Network

Different card networks charge different rates. Visa and Mastercard are known for charging lower rates. Other networks like AMEX are known for charging higher rates.

► Network partner programs

Visa and Mastercard’s partner programs like VPP (Visa Partner Program) and MPP (Mastercard Partner Program) often give specific retailers interchange rates that are much lower than the networks’ published interchange rates.

► Size of the issuing bank (𝗢𝗡𝗟𝗬 in the US 🇺🇸)

Larger banks are subject to a regulation called the Durbin Amendment that caps interchange rates on consumer debit transactions. Smaller banks are exempt.

As a result, these smaller banks can earn more revenue from interchange rates, which benefits FinTechs and embedded finance businesses that partner with them.

Source: Connecting The Dots in FinTech

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.